As I wrote about before, my early days in Singapore were sublime – particularly the years 1970 to 1979. We had a cook who churned out delicious meals, another lady to clean the house, and a devoted driver.

With no housework or cooking concerns, my time was spent doing what I loved: working with Dad in the sharemarket (with clients crowding around us hanging on our every word), and singing at night with my aunt Margaret at the Tanglin Club. We had waiters attending to us the minute we walked in, feeling the audience’s anticipation to hear us sing.

I recall reading this in Dale Carnegie’s famous book: “ … the deepest urge in human nature is the desire to be important.”1 I was happy because I was important. Then, I didn’t see a need to be good at anything else.

But when I left Singapore for Sydney in 1980, I became Mrs (Married) Average. No-one knew of my previous life. I couldn’t cook (my husband taught me how to do fluffy rice in a saucepan and roast a chicken). Food shopping scared me; I was too nervous to drive further than 10 km from home. I started work at the Prince of Wales Hospital, which was to become my second home. I held various positions there until I finally retired in June 2021.

When I first started work however, I just didn’t fit in. I thought it silly that people would talk so much about sport, recipes and planning holidays (borrowing on their credit card no less!), when they should really be discussing ways to make and save money. I hated the idea that we had to take morning and afternoon tea-breaks. How unproductive. I stubbornly chose to stay at my desk, have my snack and work. I’d be alone even on my lunch break, reading the financial pages. It’s no wonder everyone thought I was a snob and left me alone.

I became withdrawn, had low self-esteem and confidence – all because I didn’t feel important anymore. I was, however, determined to get my health right, start a family and build my share portfolio. Living from paycheck to paycheck was not what Dad told me to do.

I also knew I would never reach my potential if I continued feeling sorry for myself. But how could I reclaim my lost self-esteem?

As I wrote in my Diet & Your Colon posts, Dr Walker’s books dramatically proved my health. My son was born in 1983 and I did learn how to cook, making fresh meals for him. I tried not to be overly-critical of work colleagues, focussed on my work, and even got off my desk for small-talk during our tea breaks. This slowly broke the ice, but there was still a long way to go.

In November 1989, my sister invited me to a business meeting. It turned out to be the Amway business and people in the room were part of the ‘Network 21’ support group. Now please read on, I’m by no means introducing Amway to you!

My first thought was to excuse myself and leave. But there was something about the people there that made me want to stay and find out more. Yes, Amway had their own brand of washing powder, cleaning products, skincare and vitamins. But it wasn’t about the selling. It was about forming a network where products purchased for yourself or others in your line of sponsorship generate turnover points determining everyone else’s bonus level. The goal was to develop a business producing passive income.

I paid $55 to join so I could try the products at a discount, with 90 days to get my money back. So I bought 20 products. I was amazed at the quality and still buy them today.

Again, it wasn’t the goods, but the networking idea that intrigued me. I knew it was something I could be good at. I was impressed by the people in the room, who were so much like my father’s clients – smart, interesting and humble, And I felt comfortable with them.

I went through the Amway bonus system; it was fair. If you did nothing and your group became millionaires, your share would be close to zero. The Australian Department of Consumer Affairs said Amway was a socially responsible, ethical business. So now it was up to me.

That night I couldn’t sleep. This was a business with no overheads or compulsory inventory. Plus I had support. All I had to do was follow the Network 21 rulebook, read their recommended books, listen to tapes (cassettes then!) and go to meetings. So simple. I thought, “I can do this!”

Reality hit me. I could not build a business the way I was (ie. without self-confidence). I realised this at my very first meeting. The 7-hour long $15 seminar was actually all about GOALS. Okay, so what was a ‘goal’ exactly?? I had none.

Affirmations? Attitude? Posture? Comfort Zone? Body Language? Totally unfamiliar and puzzling to me. I felt my brain was about to explode!

A much-repeated mantra of the group was “Do what needs to be done when it ought to be done, whether you like it or not!” It stuck. DISCIPLINE. I had to acquire it.

I’m with my lifelong Network 21 friends: Uschy (left) & Anita –Sydney, 2006

In meeting after meeting with professional speakers you’d otherwise pay a fortune for, mentoring sessions, books and tapes and new diary contacts, I headed off to various homes to explain the business to my prospects. Some abruptly said, “No, not for me!” I was hurt at first, but later swallowed hard and asked, “Do you perhaps know anyone else that may like this?” “Yes!”, they said, which encouraged me to go on.

That 15-year journey was an amazing learning curve in my personal development. I learnt skills money couldn’t buy. I made new friends and contacts as my list grew – whether or not they joined me. They were people I would never have discovered if I stayed home fretting!

My involvement with the Amway business for the last 10 years has solely been as a consumer. My work at the Hospital and passion for share-investing made it difficult to be fully committed.

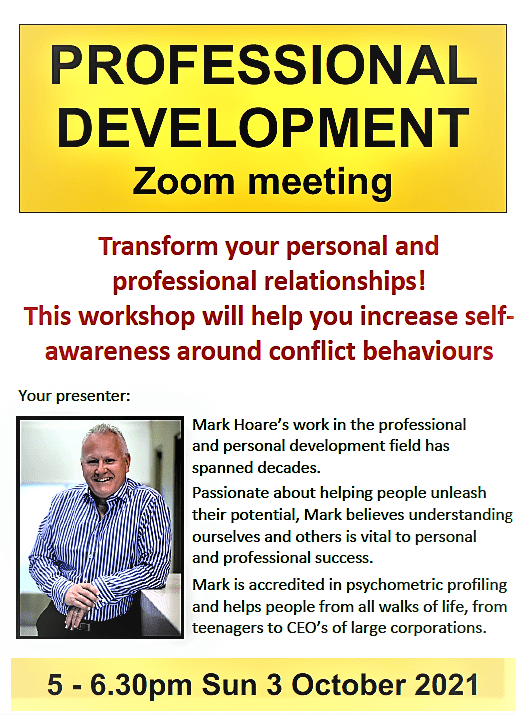

In Invest 5.0, I talked about the importance of recognising your personality and temperament, and referred to Florence Littauer’s book Personality Plus. By knowing more about myself, I understood more about people and knew how to bring out the best in them. I got so good at it! But there’s a new term now: ‘DISC Profiling’ (Dominant-Influential-Compliant-Steady).

Network 21 is hosting a free, 90-minute Zoom seminar on it this Sunday, 3 October, from 5.00–6.30pm. It’s obligation-free with no ads.

More to come on Secrets to Success in the coming weeks. See you soon!

1 Carnegie, D. [1936, 1981] (1989). How to Win Friends & Influence People [Revised edition], p.47. CollinsAngus&Robertson Publishers Limited: Pymble, New South Wales.

In this post I’ll be reviewing shares I recommended in Invest 6.0. Many thanks to Sam for contributing in part to it. He has a PhD in Accounting, and will be a regular finance and tax writer on Shirl’s Pearls.

Many shareholders, and self-funded retirees especially, received their paychecks in dividends this month. Last year was a drought for most of us – some dividends were scrapped altogether and others were reduced substantially.

Thankfully, Australian banks have recovered from the millions they paid in compensation and fines as a result of the recent Royal Commission, and the shock of the pandemic. I’m glad to report that dividends this September are (almost) back to normal!

The extended lockdowns in NSW, Victoria and the ACT may result in more ‘bad bear days’ for shareholders and super funds. Each state (apart from WA, evidently) is struggling to keep its economy alive, and some are worse off than others.

If there is the slightest risk of inflation, the Reserve Bank will likely increase interest rates; the way I look at it, from such a low base it’s not likely to hurt the property market. But borrowing beyond our manageable limits is too risky.

No-one can, or should, attempt to predict the future. Stick to the fundamentals and don’t get carried away by the hype. ‘A rising tide lifts all ships’ — but don’t be one of the dead fish on the sand when the tide goes out!

While things are still uncertain, it would be a good idea to hang on to some cash until we spot an interesting stock to buy. One such stock could be Jalna Dairy Foods (jalna.com.au), believed to be planning to list on the ASX. I like it and will keep you posted.

New listings known as ‘IPOs’ (Initial Public Offerings) of mining stocks are also coming in thick and fast. Why? Because gold, silver, copper, aluminium, nickel, graphene and ‘rare earths’ are now in demand. Everything to do with technology and quantum computing will need these materials – and there will surely be more exciting discoveries to come!

The most exciting of these materials is GRAPHENE, the building block of graphite, which has been termed a ‘miracle metal’ due to its exceptional strength (it is 200 times stronger than steel) and good electrical conductivity. As a result, graphene has many potential applications, including batteries, transistors, computer chips, medical equipment, and electric vehicles. For example, introducing graphene to the lithium-ion batteries used in smartphones and laptops has been found to make the batteries more lightweight and charge much faster than other lithium-ion batteries. Researchers are still learning about graphene and its properties, so watch this space!

The key factor with these materials is do we refine them here in Australia, or send them off to Malaysia or China for this? I would love for us to do it all. Here’s where energy supply and costs come in. I believe we’ll see reliable, emission-free nuclear energy, shunned for so long, finally up for debate.

The Sydney Morning Herald published an interesting article last August on Australian innovation. It’s not related to the stocks I’ve picked, but there are many clues that will lead you to at least 1 or 2 industry and tech stocks that are up and coming.

Meanwhile, we’re counting on the vaccine to deliver us from lockdown by Christmas. I will be so happy when all businesses – the travel and hospitality industries particularly – get their credit card and Eftpos terminals working furiously again. Don’t we miss our retail therapy? The touch and feel of what we want to buy … browsing and enjoying a coffee in a busy shopping centre … let online shopping take a back seat for a change!

A word of caution when investing in IPOs of small mining stocks (which make up the lion’s share of all new ASX listings due to the Australian economy’s emphasis on resources) – these are speculative, as they are still in the ‘discovery’ stage and have yet to start production – they don’t produce any revenue.

Watch for words describing the company’s projects as ‘exciting’, ‘significant potential’, ‘high grade’, ‘highly prospective’, ‘close to ports’ and ‘established infrastructure’ – these are all signs of a speculative investment. This means that in any given 52-week period, there is a high likelihood that the stock will at least double in price – but with an equally high (if not higher) likelihood that it will halve in price too!

My advice on speculative shares? If they are issued at 0.50c or less a share, I pick one or two which I believe have potential and buy $1,000 worth (or not more than you or I am prepared to lose). I look at the people involved and their track record: in particular, whether they have technical know-how and experience in the business. We’ll explore this in more detail in future posts.

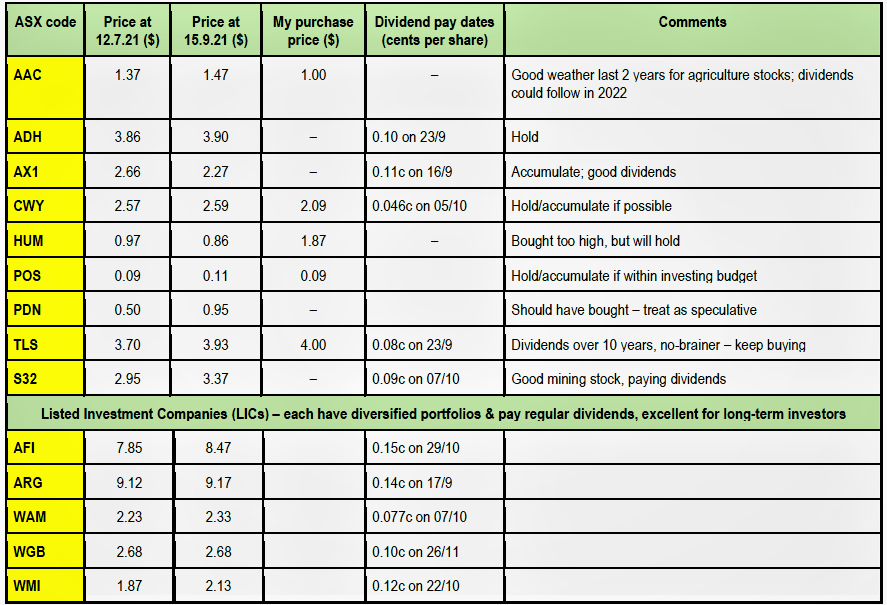

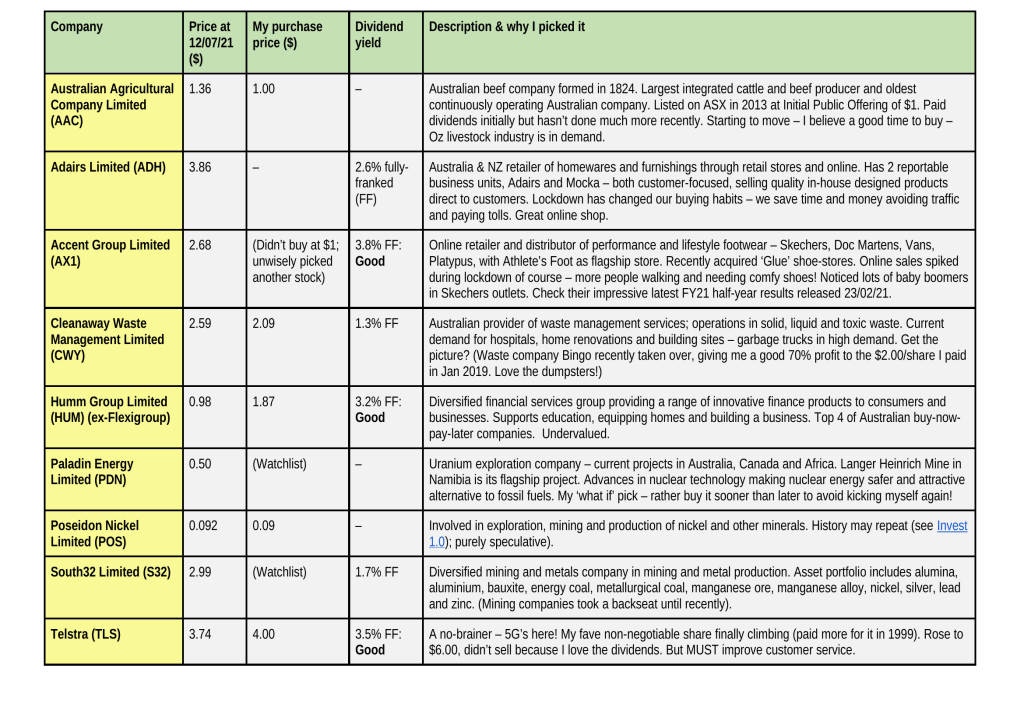

Here’s an update of share picks from the table in Invest 6.0:

I am pleased with my stock picks so far – and especially happy with the dividends! I will certainly hold on to those for a few years, Telstra especially.

Next week, Sam will help us understand the tax implications of franked dividends. Tax law is complex – but doesn’t have to be boring, and we should all learn the basics on our path to building wealth!

We lost the last link to the previous generation of our family when our beautiful Margaret passed away on 5 August 2021 in Noosa, Queensland. She was a gifted musician and singer – and a wonderfully warm, giving, human being. Her shining legacy and impact on our lives will be felt forever. This is our Tribute to You, Margaret!

‘Quizas’ by the Trio Los Panchos was a ’40s song that Margaret always sang – she loved its rich melody, Latin rhythms & major-minor key shifts

From Geoff:

I married Margaret in 1980 in Sydney, and we spent 40 wonderful years together. It was a beautiful marriage – Margaret turned my life into A LIFE! ‘I’ll Get By’ was our wedding piece, and the words of that song always remained true for us.

From left: Margaret’s brother-in-law Hans, sister Poppy, Margaret & Geoff – Noosa, mid-’90s

“I’ll get by as long as I have you / Though there’ll be rain and darkness too / I’ll not complain, I’ll see it through … ”. Our life in a song. Thank you Margaret – Much love, Geoff.

From Shirley:

Margaret, or ‘M’ as she was known, dodged the bullets of her cancer for 6 years, surprising her doctors. Her last few months were the most difficult, but she got her wish to remain at her Noosa unit to the very end. I was only an hour’s flight away in Sydney, heartbroken that the pandemic separated us. I couldn’t hold her in my arms and sing to her in her last hours of life.

Left: The Manasseh Sisters at the start of their career: Margaret (left) & sister Poppy – Singapore, late ’40s; Top centre: The Sisters on stage, New Year’s Eve – S’pore, early ’50s; Bottom centre: The reformed Manasseh Sisters: Margaret (3rd from left) & Shirley, with ‘The Constellation’ – Tanglin Club, S’pore, 1975; Right: M, Shirley & bassist David Loh – Tanglin Club, late ’70s.

I will treasure every visit I made to Noosa to see Margaret and her husband Geoff. The last time was in April this year, just before the Sydney lockdown. M gave me cassettes of all our recorded music, her scrapbook and photos. She knew she didn’t have much time left.

Sitting at her home ‘office’ table with her notes, diary, medication and TV guide, she reminisced about her life in Singapore, and the horrors of being interned during the Japanese occupation there. Her mother was widowed at 35 with 5 daughters, 2 sons and 5 stepchildren.

M and her sister Poppy worked as waitresses serving Japanese troops during the War, and also began singing together. A high-ranking Japanese officer loved their voices so much, he placed an order outside their home forbidding entry to Japanese soldiers. A lady at the restaurant kitchen gave them food to put in their apron pockets to take home. Someone was certainly watching over this family who were so vulnerable in the face of war!

The best part of my childhood was spent in my Gran’s flat (we lived in the same block), listening in awe to M and Poppy – the much-loved “Andrews’ Sisters of Singapore” – sing and play their guitars, harmonising perfectly (both learned guitar in their teens). Our beloved Poppy was just as vivacious as the pictures show, and a very good lead guitarist. She remained a crack cryptic-crossworder and witty joke raconteur right until she left us in 2013. M always felt her loss.

Singapore’s Manasseh Sisters made ‘Rum & Coca Cola’ their hit too, in the late ’40s–early ’50s

But the mid-’60s were a happy time for M and Poppy, after they settled in Sydney. They had full-time jobs, and Poppy married in 1969. My mother then insisted M should return to Singapore, saying “We CAN’T let that voice die!” (I was singing solo in nightclubs then.) M arrived in 1970 with her trusted guitar. We found a bassist and drummer, and began our career as the reformed ‘Manasseh Sisters’.

Our best and happiest times were with our band ‘The Constellation’ at Singapore’s exclusive Tanglin Club. We performed there for 7 years.

Listening to the tapes and looking back at our careers now, it’s uncanny how well our voices blended and harmonised. We had such different personalities: M lived for the moment, I planned for the future; she loved her scotch and soda, I stuck to water with sliced lemon. But on stage we were ONE. Our strengths prevailed over our weaknesses. We didn’t simply sing: M was the supreme entertainer and communicator who lit up the stage; I was the administrator who scheduled rehearsals, selected new songs and compiled song lists.

We alternated smoothly from verse to chorus if a song had a wide vocal range – and no-one could tell us apart! We all memorised our music, lyrics and arrangements. The ’70s song ‘Rose Garden’ was one that took the longest to perfect; I still recall our frustration, and then elation when we got it right!

‘Rose Garden’ was a huge favourite at the Tanglin Club

My dearest M: We celebrated your life each day you were alive. Now we reminisce and will shed many tears. You’re there in my heart and in every note I sing. I can still hear you harmonising with me. And for all those lovely years we had together on stage, I thank you!

One of M & Shirley’s last songs sung together at the Tanglin Club, 1977 – ‘Tie a Yellow Ribbon ’Round the Ole Oak Tree’

From Joyce:

Joyce & Margaret – Brisbane, 2000

It is so surreal, really, to be writing this. I don’t know where to start, because there is so much. Margaret was just here only weeks ago, and now, devastatingly, she is not. And yet … she is. Mainly because she is unforgettable. I cannot think of a single person I know who, once they met her, disliked her. It would not be incorrect to say that everyone loved Margaret.

You see, Margaret shone. As I remember her now, it’s as if she came with a light around her. She shone with deep love from within: love for her family, love for her friends, love for the love of her life, the husband she left behind, Geoff. Margaret loved life itself, the music and poetry in it; she loved making music; she fell in love with a melody, with well-constructed, meaningful lyrics, with the pathos of a love song, but also with the energizing rhythms of a Latin beat. Actually, she was so enthused about everything creative – the performance arts, unique voices, outstanding renditions, artworks. She had the amazing ability – and desire – to absorb it all.

Sister Poppy embraces the winner of the Frankie Laine Singing Competition – S’pore, early ’50s

Unbelievably it seems, this wonderful woman, my aunt, was even more: conversations with her sparkled with her wit and humor and she appreciated a good joke and told them well; her laughter was hearty and infectious. They were also filled with her insatiable curiosity about everything right to her last few days – from computers to politics to cooking and recipes, to philosophies and religion. She had an inspiring appreciation for so many things – and so many people. You always felt Margaret’s love and so, it was always easy to love her back. She was generous of spirit, she supported us, encouraged us and although she quipped, “If at first you don’t succeed – GIVE UP!”, she never did, nor did she expect us to.

She lived life her way all the way to the very end – courageously, energetically, lovingly and empathically – through a hectic childhood and being interned by the Japanese in WWII, enduring and overcoming personal hurdles to shine brighter than before, even winning, as a teenager, the Frankie Laine Singing Contest. She sang beautifully and played the guitar – and although she found it increasingly difficult to continue playing her favorite instrument, she accepted the rapidly changing situation in her life uncomplainingly. Instead, she was eager to watch ace guitarists shred the strings on YouTube. We had enjoyed exchanging clips of so many performers in this way over the years, especially so in the last few.

Yes, there is much to remember and much to write, because Margaret was involved in so much, the best you can find in a human being. In losing her, I personally have lost the most understanding, encouraging, supportive aunt I could ever have the blessing of knowing.

Rest well, my dearest M. I will always remember you with the greatest admiration and love.

From Gloria:

Margaret inspired me to strum the guitar like she did – and I learnt while watching her. Her voice was amazing, and her ear for harmony was so perfect! She recorded the opening to my weekly program on Singapore radio, ‘Let’s Make Music’, in the late 1970s. And here it is:

M opened ‘Let’s Make Music’, overdubbing & harmonising with her own voice

The Manasseh Sisters in song: M on rhythm guitar, Poppy on lead – S’pore, early 1960s

M never really gave advice; she was more focused on listening intently on what you had to say – like a ‘master listener’ – so you would always feel special to be in her presence, knowing what you had to say was very important to her. I loved her sense of humour. I miss her dearly, and can’t yet come to terms with her being gone.

Forever young in our hearts Forever young in our thoughts Forever in our music, where your music will live on for all generations to follow!

We think you’re just SENSATIONAL, ‘M’! 🎤🎶🎸

From Susanna:

I remember Aunt Margaret as a woman who loved life and loved music, and who always presented herself with so much poise. She had a gentle and loving nature. When she sang, it was with all the love that was in her heart. As we grew up in a family of singers and musicians, there was this time I specifically remember when my cousin Gloria and I (aged 13) went to a gig with Margaret and cousin Shirley who were singing with their band at the Singapore RAF Army Base. Both Gloria and I were on stage with them playing the maracas and tambourines – and we had a ball! Since that time, I learned the guitar and in no time at all, I too started playing music professionally. I would say that our music careers were really very much influenced by Margaret. I believe our families will always have singing and music in our homes throughout the generations to come.

Thank you Margaret for sharing your beautiful voice and music with us, and with so many people internationally all these years, and for triggering that spark of music into my life!

From Natalie:

(Left) M, Joyce, M’s sister Paula & Natalie – S’pore, 1978

I will always remember the first time I met my aunt Margaret. I was 8 years old, growing up with much of our family living in Singapore.

Margaret came to Singapore in 1970 for the first time since I’d been born, after she had migrated to Australia. During her visit, I happened to find a crushed dollar bill on the ground. I was so gleefully enamored and smitten by this lovely, younger and hip Aussie aunt, that I picked the dollar up and lovingly enclosed it in a ‘love-letter’ to her – in the way 8-year-olds do to family members they love. I remember how touched she was by it, and saved it for a $1 bingo ticket that week at a local recreation club. As luck would have it – or maybe it was simply the energy of love and abundance attached to the gift – she won the grand bingo prize of $1,000!

Needless to say, the whole family was treated to a lovely weekend lunch, while I was shyly designated “star of the afternoon” by her.

Margaret was a beautiful, warm, loving, smart and witty lady with a gentle nature whom we all loved!

From Efrem:

I grew up with my beautiful and elegant aunt Margaret in Sydney during the ’60s and ’70s. My childhood and teenage years were spent with her always being a living, loving presence nearby; an enduringly calm and deeply caring figure in the background of my formative life. I only ever heard kindness and encouragement fall from Margaret’s lips, and not once did she utter a hard or unkind word to me in all the years we spent together on this earth.

Efrem, M & Shirley – Noosa, 2017

After spending much time away, I had the distinct privilege of reconnecting with Margaret during her senior years in Tewantin, Queensland. Hence it was with great delight that I realized that she had grown far wiser and more insightful than I had ever known her to be. Margaret had become even more deeply loving than she was in earlier years. Her bright soul and sharp, beneficent and ethical mind shone for all to see. I knew then that the time-honored definition of enlightenment was true after all:

“True enlightenment is when a person has nothing left inside but love.”

From Dave:

Replica of M’s Akai multitrack reel recorder, 1970s

The divine, UNREAL (her pet word) ‘M’ was my aunt, godmother and mentor in music. Her rich contralto, gift for harmony, vocal arranging and multitrack recording on her Akai reel machine (as the one pictured) virtually ignited my desire to sing and perform. We both stuttered badly in childhood: singing helped us “smooth the words”. Sometimes I couldn’t even get her name out – but she always waited patiently until I did. Whilst untrained in classical music, she loved Brahms and Chopin, and would perfectly vocalise (or whistle) the exquisite melodies in Schubert’s Serenade and Chopin’s E major Etude. She always knew a “goosebump” tune or performer when she heard one!

A priceless pic of M as ‘Emma S–’, S’pore, 1960s

M had a great sense of humour and theatrics, setting me up for a practical joke when I was 4. Answering the urgent doorbell one wet night, I saw a terrifying woman with gapped buck-teeth resembling a certain ‘Emma S–’ (M was deft with orange peel). M was fun, fun, fun. At parties in the ’70s we’d play an ill-matched couple, where the tipsy husband would teeter an empty liquor bottle on his head and the wife would clutch a dyspeptic stomach.

M performing ‘If I Were A Rich Man’ à la Topol at the Tanglin Club – S’pore, 1975

She would also give a bold, powerful rendition of ‘If I Were A Rich Man’ from Fiddler on the Roof – complete with Tevye’s beard and clucks and squawks of farm birds.

In 2017, she laughingly dubbed me “Mr Fu-Manchu” for my Manchurian? moustache …

‘Lyme Regis’ flats, where Dave lived with M – Sydney, 1979

We both so loved words. I once lived with M in Sydney; crosswords were everywhere, but mostly in the loo. We did cryptics together when I last saw her in 2017, and had (polarised) political debates. She kept up with PC-tech to the end – skyping, emailing and sending us all quality YouTubes of performers and musicians. A patient listener who would intuitively interject at the right moments, there isn’t anyone who hasn’t warmed (even spilled the beans) to M’s honeyed, coaxing tones when with her in person or on the phone.

In the last few years she would always say to me how much she loved “all” her nieces and nephews, and wished “we could be together” like old times. More so in her illness, M lived in the now – as she herself sang in one of her signature songs: “Domani, forget domani … Let’s live for now, and anyhow who needs tomorrow? … ”

M’s skyped birthday message to Dave – she loved her PC & tech in general!

So for me and I know many of us, the name ‘Margaret’ will always be linked to the one and only ‘M’.

We’ll love & miss you FOREVER, Margaret … but as you often have the last word, please sing again with Shirley the song that meant so much to you!

‘Yesterday When I Was Young’ by Herbert Kretzmer and Charles Aznavour

M’s nieces & nephews – Noosa, 2017 From left: Gloria, Efrem, Shirley, Susanna, Natalie & Dave; Joyce present in spirit (not the wine)

Credits

Thank You from Shirley to:

Geoff, Joyce, Gloria, Susanna, Natalie, Efrem and Dave for expressing your thoughts so beautifully and digging deep for the photos. You have given M so much joy with your calls, emails and YouTube links to the music she loved. She got a kick out of learning new skills on her beloved computer – describing it as “unreal”!

Hans for providing a trove of photos and info about M and Poppy.

Lionel for his brilliance at restoring the quality of analogue cassette tapes and winning over digital (it’s possible).

Lina and Dave for putting this Tribute together with text, photos and audio files.

Andrew ‘The Master’ Oh for his flute on ‘Rum & Coca Cola’, ‘Quizas’ and sultry sax on ‘Rose Garden’ and ‘Tie a Yellow Ribbon’.

Noel ‘The Magician’ Elmowy from Inrock Studios Sydney, for his synthesised bass, steel drums, percussion and piano on ‘Rum & Coca Cola’ and ‘Quizas’; sound editing and final remastering on those songs, ‘Let’s Make Music’ and ‘Yesterday When I Was Young’.

Karaoke Version for backing tracks of ‘Quizas’, ‘Rum & Coca Cola’, ‘Rose Garden’ and ‘Tie a Yellow Ribbon’.

Acker Bilk & His Orchestrafor ‘I’ll Get By’ (written by Fred E Ahlert) from the album ‘Clarinet Moods’.

We’ve come to the final segment of our stockmarket adventure, where I’ll explain retirement funds and give you a selection of shares to start your portfolio.

Decide the kind of investor you’d like to be. Make it simple and narrow it down. Are you ‘conservative’ or ‘active’?I’ve made suggestions in Invest 5.0 to help you decide, so you can enhance your investment options.

Know what your financial position will be at retirement: this applies whether you’re conservative or active. It means knowing your income and expenses, which will depend on your tax bracket, mortgage repayments, and any pension and/or social security benefits you may receive.

Know your tax threshold according to your tax bracket. The Australian Tax Office provides details of individual income tax rates. Saying “I can’t get my head around any of this!” will not get you far – you will never understand if you don’t take the time to find out. BUT: if you need an accountant to sort out your tax, get one.

Buying & keeping shares

Having started so early, the sharemarket is now my second language – but what I learned in the 60s and 70s was not complicated!

We bought dividend-paying ‘yield’ stocks, giving us a good income

Saw new opportunities in ‘growth’ stocks

Picked 10 of those growth stocks and discussed them with our groups

Traded and waited.

Some of my shares took off within months, others after years; four would die a slow death. Still believing they could be resuscitated, we have this bad habit of clinging on and not selling even if the share/s make up just a fraction of our portfolio. Psychologists believe our reluctance to take a loss is greater than accepting a gain. Very true!

TIP: If your stock falls, say by 10–20%, it may be a good idea to get out of it quickly. As long as you can show profits from other share trades in your tax return, you can also off-set losses.

Internet & media

The internet has now made investing easier. We simply click to buy, sell and research without having to talk to a single person or see a stockbroker. But the noise-info from financial ‘experts’ and economists has overwhelmed and confused many of you. Notice that their predictions are always accompanied by “maybe”, “most likely”, and/or “if management continues on this growth trajectory … “ Is this at all helpful??

The fact is nobody knows the future and profits generated the year before may not continue to the next. Have you picked up how the media, right on target,come out in droves when there’s a ‘bear’ market crash? They simply love the chance to go on TV or social media, telling you how much the shares have fallen and how much your superannuation has dropped. And they do the opposite when shares rise sharply in a ‘bull’ market – crying “it’s boom time’’ rattling off the stocks that have risen so much, it makes you sick that you didn’t ‘get in’ earlier!!

You know what? WEcan do much much better.

Spend-control

First remove the fear of investing. I get it that most of you are clinging on to your hard-earned savings, earning a measly 1% interest. Let’s put spending in perspective.

In the past year, how much have you ladies spent on toiletries, fragrances, shampoos, and skin-care? Clothes, shoes, accessories? Cleaning products, cookware, kitchen gadgets? And how much have you men spent on electrical gizmos, computer games and equipment, and sports gear? Have we actually used every single item of stuff we’ve bought?

And then there’s eating out. Have we splurged on decadent breakfasts or lunches where only 1 serving costs more than an actual dinner? Have we bought presents thoughtlessly? We often give kids rubbish. Why not deposit money in their bank accounts?

Calculate all your misspends. Excluding food you’ve thrown away, what does it come to in the course of a year? We don’t give a thought to the money we’ve wasted but focus instead on the money we may lose!

My father and his friends would frown on such thinking. They invested wisely with thousands, but avoided supermarkets for Singapore’s (clean) wet markets – buying fruit and vegetables dollars cheaper per kilo.

Managed funds

You might be feeling complacent with your superannuation and other managed funds without getting more involved – but you should read your fund’s annual financial report. In particular:

How your fund is performing

Management and investment fees charged

How and where your money is being invested.

Invest in at least 1 online daily newspaper – they’re quick to alert of any argy-bargy with investment products.

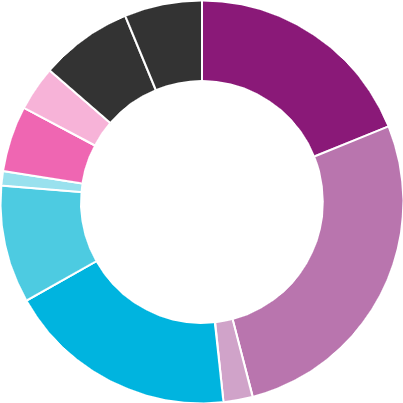

In a superannuation portfolio for example, you’ll usually see a pie-chart divided into coloured segments totalling 100%, showing where your money is being invested. Fund managers will alter percentages according to market changes in the short to medium-term. Here’s the pie-chart of my own super fund:

Equities: Shares

Private equity: International or Australian companies unlisted on stockmarkets

Cash: Safe and secure with low risk, giving 2–3% interest

Australian Fixed Interest: Bonds loans issued by the Australian govt – less volatile than shares but lower expected return

International Fixed Interest: Bonds as above

Credit Income: Covers a range of alternative debt investments

Infrastructure & real assets: Utilities & facilities providing essential community services.

TIP: Click the ‘Asset Classes’ link on your super fund’s website for more information.

Superannuation funds usually give you 4 investment options:

‘Cash‘

‘Capital Stable‘

‘Balanced‘

‘Growth‘ .

Cash, Capital Stable and Balanced are safer for those in or near retirement, safeguarding income from regular allocated pension payments in any sharemarket crash.

Growth means share investments for younger people with time to recover after a downturn. It’s still important to have the Growth option in all portfolios. When the market recovers, you don’t want to lose out by having all your capital staying in ‘safe’ mode.

TIP: If super funds bidding to buy Sydney Airport are right, there’ll be a substantial revival in both local and global travel.

A few of my own ASX picks

FINAL TIPS:

Avoid travel stocks WEB, QAN and HLO at present – but keep watch. Every living being with money saved up will be packing their bags to cruise and fly once vaccination rates go up and that awful green spiked ball disappears from our screens.

Keep up with business news in your daily papers and online. Subscribe to at least 1 of Motley Fool’s many specifically targeted newsletters (eg. ‘Share Advisor’, Extreme Opportunities’, ‘Dividend Investor’ or ‘Hidden Gems’).

Observe. Talk to people. You’ll develop a keen sense of what the future holds. Therein lies the secret to share investing. Simple enough?

“TIME IS MONEY. BUT WEALTH IS THE RESULT OF TIME.”

The perfect quote from Scott Phillips of The Motley Fool to end my About Investing series (for now). I simply loved presenting it to you – GOOD LUCK!

Do you realise that your personality type is critical to your initial and ongoing capacity to invest? It’s so close to home, yet it’s one thing we overlook (or choose to).

Maybe I should distinguish between personality and temperament.

What we all see is your personality: it’s the face you put on. But your temperament is what you are underneath.

I first learned this in the book Personality Plus by Florence Littauer – a delightful author whom I actually met at a seminar 30 years ago. Reading it made me realise how important it was to understand our inner selves, as she writes:

“Know what what we’re made of know why we react as we do Know our weaknesses and how to overcome them.”1

This jazzy, fun chart compares the 4 temperaments we apparently have:

Similar to the chart, Littauer says:

The sanguine’s “optimistic, cheerful and bubbling”

The melancholic’s “analytical, detailed, perfectionist”

The choleric’s “adventurous, confident, productive”

The phlegmatic’s “patient, obliging, consistent, laid back”.2

Decide which temperament you are – but you could be a mixture of them!

Littauer also gives us a very thorough checklist of strengths and weaknesses to determine our dominant and less dominant personality traits. Please get her book if you can (it’s had numerous reprints).

So it’s quite clear that by understanding ourselves,we learn to understand others – so important in business and personal relationships. But it’s especially important in INVESTING, where your temperament is key to your ability to make right decisions.

TIP: Want to be successful? Work on your weaknesses and enhance your strengths!

My dear Dad, in his innocence, knew this. He matched stock recommendations with what he called his clients’ “moods”. Here’s one example.

A wealthy, well-known lady – we’ll call her ‘Patsy Leow’ – used to frequent the Singapore Turf Club in the old days. She loved picking ‘outsiders’3 – but most of her money went on horses with short odds, or ‘favourites’.

Gorgeous Madam ‘X’ is a dead-ringer Patsy Leow!

When Madam Leow asked Dad for his share tips, he chose those “that will never go down” – solid companies with increasing yearly profits and paying healthy dividends. He also told her of 2 or 3 shares he liked that were “cheap now but had lots of potential to go up in price”. Her eyes lit up and she said, “Yes, Alex, we’ll put a few thousand on those!”

Such speculative stocks kept Madam Leow interested: she liked the challenge and excitement in picking a winner that would eventually pay well, and she came back for more.

So for all you optimistic choleric and sanguine risk-takers – who enjoy a good punt and love to talk about your wins, ‘speckies’ have great appeal, and you’ll likely go this way.

But worrying melancholics and laid-back phlegmatics amongst you should invest conservatively, limit borrowings and stick to topping up superannuation, investing in property, managed funds, and ETFs or LICs (see Invest 3.0). Such options will suit you perfectly without the compulsive need to check your stocks several times a day!

In the past, worriers bought “solid” shares which they could “lock up and keep for their children”. It worked well 20 years ago, especially for the banks, but not now.

I also recall a manager of the Hongkong and Shanghai Bank pointing to me when I was 8 and saying to Dad: “If you love your daughter, buy her HSBC shares!” My father did more than that – he also bought shares in Standard Chartered Bank, and told his clients to do the same.

TIP: Banks are no longer stockmarket darlings. ‘Fin-techs’ – a common, current term – relate to digital financial products like ‘Blockchain’. This is looming to weaken dominance of the Australian ‘Big 4’. It’s time to look for other dividend-paying stocks with growth potential.

My personality, my formula

My personality without a doubt influences the shares I buy. But it’s a little more complex. I believe I’m mainly sanguine with a little of the choleric, melancholic and phlegmatic thrown in.

I love excitement. I’m a risk-taker. I love the unexpected. But at the same time, I’ve learned to be patient and cautious.

My strategy over the last 40 years was to slowly build my portfolio up to about 30 stocks, and sometimes more. This roughly comprises:

50% per the ‘IPD’ formula (see Invest 1.0) that tick boxes of income, profit and dividends

30% into ‘growth’ stocks with healthy revenue (ie. income before expenses), but haven’t yet made a profit (ie. income after expenses)

20% in reserve for stocks with ‘potential’ – but I don’t invest more than $1000 on those. While no-one wants them today, I’m thinking long-term for up to 3 years.

My advice

Don’t get caught by the FOMO (Fear Of Missing Out) – it’s dangerous!

Assess how much you can invest. Never, never, never over-borrow to buy shares.When the market dives, you’ll still sleep well. The good news is markets always recover. If you’ve invested wisely, your money’s safe. People who’ve told me, “I’ll never buy shares again!”, are those who were bitten by the FOMO bug. They lost their money, their pride, but worse, missed opportunities yet to come.

TIP:Be patient. There will ALWAYS be a good time to buy. Keep saving and make sure you’re mentally, physically and financially ready to ride the next wave. Happiness isn’t having money, but peace of mind and sleeping well at night.

What should you invest in?

For those about to retire, my best advice is to top-up your superannuation to the max while you’re still working. If you want to have a go and have a spare $1–5K, get Telstra (TLS) and another newish Telco I’ve heard good things about: Aussie Broadband (ABB). TLS has a decent and fully franked dividend. (I hold parcels of Telstra and BDA, I’m watching ABB and may buy soon.)

Want some fun? There are 2 (shock, horror) marijuana stocks you could pick: BOD Australia (BDA) and Althea Group Holdings Limited (AGH). Prices as of 5 July 2021 are 0.37 cents and 0.35 cents respectively. I believe you’ve a fair chance of making a profit in a year. I hold parcels in both shares.

If you’re not ready to start an online trading account, the ASX website is excellent. You can create your watchlist and monitor and research stocks. It also runs several information sessions throughout the year.

Worriers should go for managed funds or ASX-listed investment companies (LICs). I’ll give you the ASX codes for some LICs and leave you to research them. Pick 1 or 2 and don’t look at their prices for a few years:

–AFI –ARG – WAM – WGB – WMI.

You can see that I find all this very thrilling and engaging – I hope you also do by now! That risk element is the motivation we all need to keep us researching, observing and asking questions.

I’ll share my vision for the future with you in Invest 6.0.

1 Littauer, F. (1992). Personality Plus, p.12. Grand Rapids, Michigan: Baker Book House Company.

2 Littauer, p.19.

3 What we call ‘long shots’ or ‘roughies’ – ie. horses unlikely to win.

4 Stockbroker-speak for companies presently sitting in a corner waiting for someone to ask them to dance. Will they eventually take to the dance floor? In my experience, even when only 1 or 2 of them did, I more than made up for those that packed up and left!

I’m now going to get quite personal with you. How does your lifestyle affect your ability (or inability) to invest?

My advice to you is to first take stock of your everyday life. Are you too busy to pay attention to your health?

In my 20s and early 30s, I ate anything and everything that was ‘easy’ and required the least preparation. I didn’t have an exercise routine and lacked energy and concentration – not good when you have a family and are trying to build a second income.

What have I realised since?

A regime of healthy eating, exercise, good sleep, social interaction at work and with family and friends sharpens your senses, keeps you motivated and inspires you. Importantly, it lifts your attitudeto become open to opportunities and make rational decisions with your money!

When I look around me, I see many people who frown and seem distressed, worried and anxious. I smile at (mostly) everyone, but no-one smiles back! I get a certain pleasure in doing this because when even only one person reciprocates, it’s as though I’ve made their day. And often the sad faces I see and meet are those with money problems.

If this is you now, don’t gamble, invest or make any financial decisions, however attractive the ‘sure thing’ looks. Simply wishing you had more money won’t get you out of this hole. You need to solve your problem quickly.

What should you do?

If it’s your health, seek professional advice. Don’t make excuses, or try to figure out what’s wrong with you.

If it’s your finances, seek professional help or ask someone you know who can guide you in this area. A good Australian resource is the ACCC1 : its ‘Where to get help when you’re in debt’ guide is excellent. It’s important to remember that when you’re feeling ‘low’, you become vulnerable to get-rich schemes that promise ‘instant’ gratification. Gambling, buying shares or investment plans you know little about is DANGEROUS.

You might be in a troubled relationship – whether intimate, with family or with friends. I believe this is the hardest to reconcile and fix. Whether we like it or not, our lives revolve around those nearest and dearest to us.

Is your work situation happy or unhappy? I know I couldn’t possibly turn up for 8 to 10 hours a day working in a place that made me miserable. Anyway, I wasn’t ambitious, because the people ‘higher up’ the chain didn’t inspire me.

My first and last permanent job (which lasted 35 years) did not pay a 6-figure salary that my colleagues aspired to. But I LOVED IT. My goal was to build a second income (my Dad’s advice!) and get home in time to make healthy dinners for my family – not to attend endless meetings, compile reports and spreadsheets. This wasn’t my thing and bored me senseless.

Building wealth

Now, that excited me! Reading the business sections of newspapers, talking, listening and observing with the objective of finding the next share to buy.

When life took a beating, I took a deep breath. I didn’t trade until things went back to normal and I could make rational decisions again. The best part was that because I saved, invested and built my portfolio, it was earning dividends: I could always sell 1 or 2 shares without having to borrow on my credit card.

Do you dream of being happy, healthy and focused? Your lifestyle determines your wealth or lack of it.

Nothing runs smoothly in life. When there’s a bump on the road, will you grumble and crumble? Or will you be IN CONTROL?

Well … here’s where your PERSONALITY comes in, in its close link with your lifestyle. Invest 5.0 will explore this very subjective but important element.

Can I assume that by reading this far into ‘About Investing’, you’d like to learn more about the sharemarket?

If so, I hope you’ve now started to save. You need a minimum of AUD500 to buy an ASX-listed company. Add up to about $30 for brokerage costs and GST charged by the online trading platform. (Charges might vary according to the broker.)

There are 3 important things you need to take into consideration:

AGE

LIFESTYLE

PERSONALITY.

I will deal with the age factor in this post.

Age

This is crucial as to what shares you buy, whether you want income (through dividends) or growth (stocks that have potential to increase and grow your money-tree).

1. 19 to 25 years

You’re probably spending too much of your parents’ money and too much time on your devices!

When I was 20, I was already well-acquainted with the stockmarket. It was 1969. Newspapers were full of the astonishing rise of a West Australian nickel company called ‘Poseidon’. Nickel was in great demand from the 1960s due to the Vietnam War. From 80 cents a share in September 1969, Poseidon went up to $280 by February 1970. Some brokers even said it could go up even further. (Advice: Brokers and ‘experts’ often get it wrong!)

Poseidon has in fact been resurrected. But will it take off again?

TIP: Nickel (Ni) is in demand again, 52 years later. This ‘power metal’ is used in all things electronic – batteries, electric vehicles, smartphones and medical equipment to name a few.

TIP: The world’s largest producers in order are: the Philippines, Russia, Canada and Australia. Pay attention to the nickel producers that have binding supply contracts (i.e. they’ll be there a lot longer).

Finally, 19 to 25s – please read my last 2 Invest posts. You have the precious gift of time. You’re smart. Use your intelligence wisely. Social media influencers won’t make you rich. The sharemarket will.

2. 25 to 39 years

I know you really want to buy property – but that could well be beyond your reach, especially in Sydney and Melbourne.

There are many more people like you discovering the advantages of entering the stockmarket. You’re listening to podcasts from experienced investors. You’re online, continually searching for ‘tips’.

But too much information results in confusion.

Balance your information and your index funds with your own research. Spend a little of your investment money and buy 1 or 2 of your own stocks! Get excited about them! I guarantee it will help you better understand the mechanisms of share movements.

‘LICs’, ‘LITs’ and ‘ETFs’ … I hear that you talk about them a lot. They’ve become ‘trendy’. But do you fully understand the difference between them and ordinary ASX-listed shares? Read this Q&A article by Andrew Heaven (The Weekend Australian, November 7– 8, 2020).

Google should not be your only resource. OBSERVE what’s around you. So many clues! Get together with like-minded friends. Pool money together to buy investment magazines or subscribe to excellent resources like The Motley Fool and Padley Today. TALK to people.

If you’re still keen on property in Australia, it’s still an option in South Australia and Western Australia, and even in country NSW and Victoria. The same principle applies to shares. Finding the next best thing or the next best location is worth the time you spend researching and asking questions.

Lastly, SAVE. By all means go out for your coffee, but stay in for your smashed avo on beautifully toasted sourdough!

3. 40 to 55 years

This is a critical time. Think of how you’d like to spend your retirement.

If you’re working, put as much as you can into your mortgage (if you have one) – and depending on your income, opt to salary sacrifice up to the maximum allowed.

Don’t be blasé about your superannuation or finance. Get the facts now, not when you’re 60!

Most super funds have financial advisers, and some may not charge for their initial consultation. If you want to keep it simple, pick a good-performing fund and keep an eye on it.Websites have links to compare fees and performance with similar industry or public super funds. The Australian Taxation Office website is also helpful. Read the PDS (public disclosure statement) that all super funds must provide; if there is anything you don’t understand, ask.

There’s a marvellous article by James Kirby in The Australian about financial advice and the fallout from the recent Australian Hayne Royal Commission. He notes financial advisers are now harder to find, and says:

“ … This is a sector in crisis. Industry reports suggest that the total number of licenced advisers will drop from 22,000 to 15,000 over the next few years. …

“Due to the burden of post-Hayne financial advice regulation the best advisers want to concentrate on ‘sophisticated investors’ who operate with much less ‘red tape’ than everyday investors. That is, they satisfy the legal definition of ‘sophisticated’ having $2.5m in investable assets or an annual salary of $250,000 a year.”1

In a nutshell, Kirby writes that you need to invest $500K to be considered a worthwhile client. To make an adviser’s practice viable, they must be able to charge you $3000 a year (at least). What’s more, paying for one-off (or “niche”) advice you need at the time (which to me seems perfectly reasonable and fair) is not possible under current rules in the industry.

So unless you’re resigned to paying $2000 to $3000 a year for a financial adviser, “that’s your lot!!” (a phrase of our senior gardening guru, Peter Cundall).

BUT … if you’re willing to use $1000 or more of your savings, I encourage you to buy shares. Read my previous Invest posts. If you have any questions, please leave a comment at the end of this post, or in Let’s Talk.

4. 55 years & over

You should have already set a retirement date!

Barring any unexpected events, have an idea of how much super you’ll have and the tax-free income you’ll receive.

Personally, I don’t think ‘retiring’ is a good idea.

TIP:Your last day at work must be the first day of your new life!

What can you do now that you couldn’t do before? NEVER stop doing what you love: keep meeting with friends, make new ones, learn a language, musical instrument, join a choir and … a gym!

Invest 4.0 will explore how your lifestyle and personality impact on your ability to invest successfully.

1 Kirby, J. (June 5, 2021). ‘This year’s advice: Rip it up and start again’. The Australian.

My many years in payroll at a major Sydney hospital made me aware of one thing: most people spent more time worrying about their fortnight’s salary than their financial future!

Women in particular didn’t “want to be involved in anything financial”. Most did not know how much interest they were paying on their mortgages, or what their credit card balances were.

From married women, I’d often hear: “I just let my husband or partner handle our money – I don’t understand anything about investing.” And from single ladies: “I’m too scared to buy shares – I just put my money into super!”

Ladies: Learn to invest for yourself!

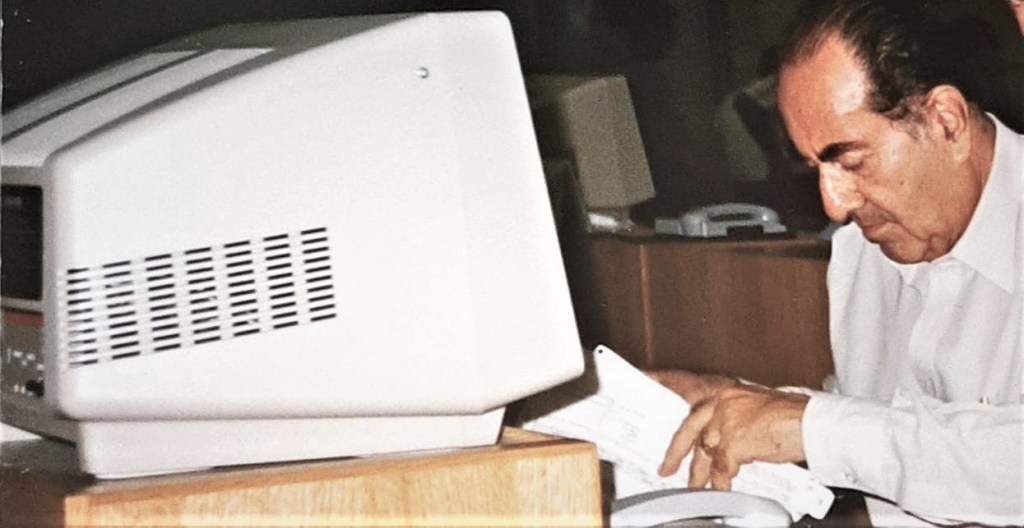

The trend was so different in Singapore. At my Dad’s stockbroking firm, clients actually comprised more women than men. They would come in at 10am sharp with their pencils and notebooks to exchange share-scrips and deal out their ‘chits’. They did their homework and were ready to trade. My father, Alec, was their favourite broker. He was honest, and would refuse to take their orders (and anyone else’s) if he thought the shares were “rubbish”. People listened because most of the time he was right.

Respected 73 y.o. stockbroker Alec at the office – S’pore, 1987 (he loved his PC too!)

Dear ladies, relying on one person to secure your financial future and/or burying your head in the “it’s all too hard” box is not an option – especially in these economically uncertain times.

Men: this goes for you as well. Responsibility of managing money must be shared or at the very least explained to your partner who doesn’t want to be “involved”. Broken relationships, unexpected illness or death can result, and the other partner might be made homeless or be scrambling to make sense of paperwork left behind.

You can learn basics of tax and investing!

Unfortunately, there aren’t as many wise and honest stockbrokers these days like my father. But the good news is that we can do it ourselves with online trading platforms like CommSec. It’s simple to buy and sell shares on it, and easy to navigate too. You simply can’t miss the BUY and SELLclick boxes! Research before you trade – and with a steady hand on the mouse, your confidence will grow and you’ll make sensible decisions.

Ready to trade online?

Get a Scrapbook

What’s your goal? Is there more than one? Why and when do you want to achieve this? Write it down.

What’s your dream? Write it down. Your goal needs to be strong enough to stop you frittering away your time on things you needn’t be doing at all. I knew my dream from age 8, and I still have my Scrapbook – I’ve never stopped cutting and pasting articles on shares in it. (My dream was to sing in a band, so I kept writing a list of songs I liked. I also wanted to be smart like Dad and learn about shares.)

We do have time. In fact, lots of it.

Write a share-list of what you think will be the ‘next best thing’ in the future – and get their ASX codes.

REMEMBER: Investing is for the long-term. It’s too late when shares have already become a ‘trend’ (e.g. Afterpay), when prices keep rising and it’s too costly to buy.

Start an online trading account. If you’re unsure which, the Commonwealth Bank’s CommSec platform is a safe bet.

Start a watchlist of share codes of shares you like. Each code will have its own company info and updates. Annual reports should be the first thing you read. If you don’t understand what the figures mean, look at the profit, loss and turnover figures. Easy enough?

Read, read, read. Subscribe online to The Australian, The Sydney Morning Herald (includes The Sun-Herald) and the Australian Financial Review. Later, I suggest you subscribe to a few newsletters from The Motley Fool, e.g. of the ‘Dividend Investor’, ‘Share Advisor’ and ‘Extreme Opportunities’. ‘Marcus Today’ is also good, and a useful guide to your existing stock picks.

Observe. When you’re out shopping, what are the ‘BNPL’ (Buy-Now-Pay-Later) options advertised? Okay, maybe it’s too late for Afterpay, but there are still others under the radar doing well; you’ll see their names if you look for them when shopping.

Ask questions. Speak to your friends. What are they buying? Clothes, make-up, furniture, home appliances, computers, TVs? Is it online or from retail outlets? What are their best or best-avoided sellers? Behind each product is a company, and behind each company is an ASX code.

Network. Find 4 or 5 people that have an interest in stocks and shares. Get together whenever you can and brainstorm – it’s so much better than an online chat room! Start conversations. Expand your network. I got my best share and property tips from people I never knew before!

Learn the terminology and acronyms. Here’s a list to start with:

– Franking credits – Ex-dividends & Cum-dividends – Options – Rights issues – IPOs – SPPs – SAAS, IOT, SMB, A1 (new terms in annual reports for tech-based companies).

I’ll stop now, your head must be spinning. Thanks for bearing with me.

Invest 3.0 will have more ASX codes to research and one very important factor many financial advisers miss … PLUS the many mistakes I made which I want you to avoid!

Okay, it’s not only about stocks and shares – but in 1950s idyllic Singapore, it was the only thing Dad (and everyone we knew) was doing. Every morning from the time I was 8, I’d sit next to him, with his newspaper spread out on the dining table. He’d read aloud names of his rubber, tin and palm oil shares to me, and would listen to share reports on radio every weeknight.

He went further – giving reasons why he bought them and why he knew they would go up in the future. “Dad will make lots of money to start his own business and Mum won’t have to go to work!”, he’d say.

At the time, ‘money’ and my mother not having to work held special meaning for me. My parents frequently argued about finances and Mum always looked tired when she got home late from the office. Yes, we had our devoted nanny (Ah Chai) to bathe, clothe and feed us – but I so wanted my mother there too. Dad’s vision appealed to me: I was interested and wanted to know more.

Enid Blyton and singing in front of the mirror now took second spot after I started reading the financial page in Singapore’s Straits Times (I write ‘page’ because they had only one then), and later the Business Times. I don’t remember Dad reading anything apart from this newspaper and annual company reports. He told me it was important to read them and check on their income, profits and dividends (IPD). Losses are not necessarily bad he said, if the company was growing and expanding – but if income and turnover kept increasing without a profit, “Be careful!”

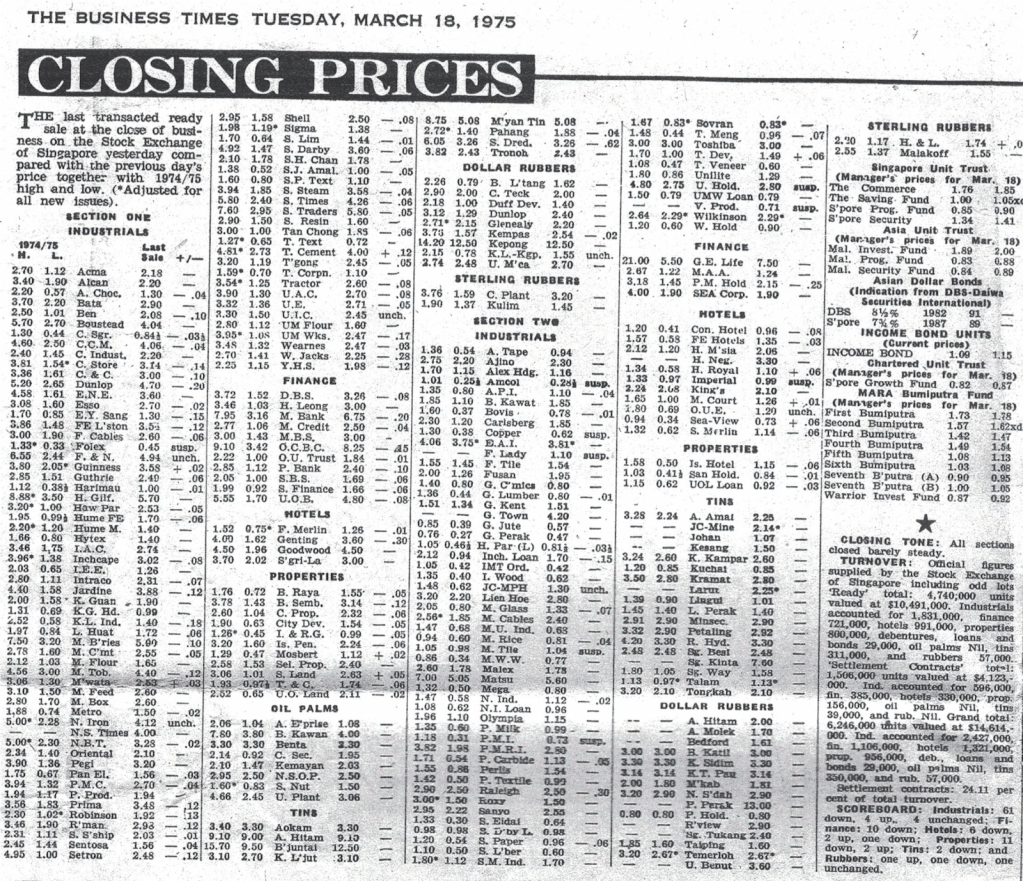

Closing share prices from Singapore’s Business Times, 1975 (my daily staple)

Our home slowly became what we now call a ‘chat room’ with one exception: food and people were included. Our live-in cook and maids diligently served and cleaned while Dad exchanged share-scrips (or the colonial term ‘chits’) with his clients. Some stayed for a meal, others sat and talked. I listened. I made notes.

So that’s what I learned early on about the ‘secrets’ of investing. While I believe nothing much has changed, I encourage you to heed my father’s warnings so you’re well prepared.

Moving forward to the 1980s … my ‘quiet’ years, compared to the bustle-buzz of my Singapore days. Adapting to my new life in Sydney, I had only(!) 3 goals: paying off the mortgage, starting a share portfolio and buying an investment property. Do you notice that all 3 were finance-related? What finance gurus preach now, I did then – no eating out, movies or shopping for things I didn’t need.

I SAVED. I INVESTED TIME. I PREPARED.

I already had a few ASX stocks in my portfolio by then, but needed more. I read newspapers but didn’t buy them – mostly because I snatched the loose business sections that people had thrown out in shopping centres!

But I did subscribe to the magazines Money and Share Investor. I now subscribe to The Motley Fool run by Scott Phillips. I also read Marcus Today, partly because I fell in love early on with Marcus Padley who just happened to give the same advice my father did …

I picked apart the stocks recommended in the magazines and newspapers, highlighted and then wrote down what I liked in my ‘share book’. In 2 years, my savings were growing nicely and I would soon be ready to launch my portfolio.

I know that times are tougher now – it’s so much more difficult to buy an investment property than it was 20 years ago, especially here in Sydney, even with low interest rates. But here’s where shares come in: banks will be paying near-zero interest until at least 2024, so it definitely pays to do your research and build your portfolio.

10 tips to start a share portfolio

Get the necessary information about the companies, including their ‘IPD’: income, profit and dividends.

Have patience and courage to begin.

It’s OK to borrow money to buy shares (or a property) – but have enough for you and your family to live on, and don’t borrow so much that you can’t sleep well at night.

Never spend more than you earn.If you can’t pay off your monthly credit card balance, you’re spending too much.

Ask advice from those smarter than you, and take them out for lunch!

Save regularly even if it’s a small sum – you’ll be rewarded.

Never believe anyone who boasts of a ‘fortune’ they made on the stockmarket. They’re either exaggerating or lying.

Choose value over cost. Don’t avoid shares simply because their price is too ‘high’. Buying 100 shares at $10 each may give you a better return than buying 1000 shares at $1!

“What can you see that no-one else can?”1 Take your eyes off your smartphone and look around you.

“If you’re good in this game, you’re only going to be right 6 times out of 10. If you buy only 1 stock, you’re essentially tossing a coin and that’s no way to invest!”2

We’re now entering the decade of 5G. Are you aware of how much it will impact our everyday lives? For example in health, agriculture, transport and e-commerce? Quantum computing, smartphones, electric cars – what do they need? Lithium, graphene, copper and nickel. Make a list and pick 1 … or 2.

Please watch my previous ‘Let’s talk finance‘ snippet if you haven’t already.

Don’t be afraid to start. Focus. Time is your friend, don’t waste it.

Finally, because I love linking my posts: IF YOU EAT BETTER, YOU’LL THINK BETTER!

Stay tuned for Invest 2.0 out soon.

1Padley, M. (November 8, 2017). The Sydney Morning Herald.

2Phillips, S. (January 6, 2021). The Motley Fool Share Advisor [Scott Phillips quotes Peter Lynch].

I first heard about menopause and osteoporosis in my early 20s. It was in a book called Everywoman by Derek Llewellyn-Jones, which my prudish mother kept hidden. I found it by accident and read the contents.

‘At a time which is quite variable and individual for a woman, the remaining egg follicles in the ovary begin to disappear. This … occurs sometime between the 45th and 55th year of life. …

‘As the months pass fewer egg follicles are stimulated and the amount of oestrogen secreted by them diminishes still further, until the menstrual periods cease altogether. The menopause has arrived. … [T]his is a time of hormonal turbulence.’1

And:

‘Hot flushes are noticed by at least three-quarters of women … other symptoms often attributed to declining hormones include depression, irritability, headaches, palpitations, dry skin, frequency of passing urine.’2

Llewellyn-Jones believed that those symptoms were not because of a lack of hormones but because of the need to adjust to being menopausal.

Osteoporosis

‘Women lose bone more rapidly than men, particularly 5–10 years after the menopause. The thinning of bones is called osteoporosis.’3

Right. So this was what I had coming to me? The price I had to pay for being a woman? Why didn’t Mum at least warn me?

But thinking of it now, how does a mother explain to her young daughter what she should be preparing for when she reaches 50?

Maybe I was different. I wasn’t into clothes, make -up and the usual feminine ‘things.’ All I wanted was to learn how to stay healthy, sing, write and be financially independent. At 20, I was already thinking of the future – mainly spelled out by slogans from my Dad such as ‘save’ and ‘buy shares. Health was the last thing on my list – until after I turned 30, when I was first drawn to the books of Dr N W Walker.

As it turned out and discussed in Move! 2.0, I had premature menopause at 36. I knew osteoporosis would cripple me if I didn’t take steps to prevent it.

In reality, would young, beautiful, vibrant women today even believe they should be preparing now for this ‘thing’? I think most would google ‘menopause’ or ‘osteoporosis’ and then promptly scroll back to their favourite websites.

My early symptoms were:

less frequent periods with longer intervals between

insomnia

rapid heartbeat

frequently dropping things

dry skin

brittle hair without body

general lack of interest in life.

One night after months of tests, totally discouraged and frustrated without any conclusive diagnosis given, I sat on the floor crying, wishing, praying, and hoping I’d find an answer.

The answer came the next morning. I remembered what I had read 14 years ago, and asked my doctor for a blood test to check my FSH (follicle stimulating hormone) levels. I already knew what the result would be: yes, it was menopause. I was just too young for this!

The somewhat encouraging words from my doctor were: ‘No more children, Shirley – but at least you have your son.’ I sat on a park bench and cried some more.

The disturbing images of old age I had growing up in Singapore flashed before me: I now fully understood. The men and women who couldn’t get up from their chairs, who gorged, didn’t exercise, smoked, drank and sat all day. They only looked forward to heart disease and diabetes.

In Move! 3.0 I wrote on how HRT restored my life again. But I knew I couldn’t depend on that alone. It was Diet, Exercise, and Relationships. And I had to work on all 3.

HRT – plus …

I keep returning to this topic because I’d like my female readers to avoid the pitfalls I met.

My first question is: is it the true fountain of youth it’s made out to be?

Many friends have suggested that it’s a substitute for exercise. They tell me: ‘It’s alright for you – it’s HRT that’s giving you energy!’

But HRT alone does not build bones and muscles or release endorphins. It can also make you put on weight.

If not for Dr Walker’s diet, eating more calcium-enriched foods and sticking to my food combinations, I would have easily piled on the kilos over the years. It was also years of walking, my mat home-exercise and more recently, the regimen of a structured weights/aerobic circuit class at the gym.

It was HRT, my DIET and EXERCISE that saved me from osteoporosis.

I also found HRT’s effectiveness diminishes with age. When the time comes to stop taking them (around 75 years) I want to walk away with confidence, still active and enjoying life – and not as a wobbly, crotchety old woman.

So dear friends, please remember it is never just the one thing that gives results. It could be the foods we eat, friends we choose to have, or the way we think. With the right options, YOU are the creator and YOU are in control.

1Llewellyn-Jones, D. (1971/1992). Everywoman: A gynaecological guide for life [6th edition], p.379. Penguin Books Australia: Ringwood, Victoria.