We’ve come to the final segment of our stockmarket adventure, where I’ll explain retirement funds and give you a selection of shares to start your portfolio.

- Decide the kind of investor you’d like to be. Make it simple and narrow it down. Are you ‘conservative’ or ‘active’? I’ve made suggestions in Invest 5.0 to help you decide, so you can enhance your investment options.

- Know what your financial position will be at retirement: this applies whether you’re conservative or active. It means knowing your income and expenses, which will depend on your tax bracket, mortgage repayments, and any pension and/or social security benefits you may receive.

- Know your tax threshold according to your tax bracket. The Australian Tax Office provides details of individual income tax rates. Saying “I can’t get my head around any of this!” will not get you far – you will never understand if you don’t take the time to find out. BUT: if you need an accountant to sort out your tax, get one.

Buying & keeping shares

Having started so early, the sharemarket is now my second language – but what I learned in the 60s and 70s was not complicated!

- We bought dividend-paying ‘yield’ stocks, giving us a good income

- Saw new opportunities in ‘growth’ stocks

- Picked 10 of those growth stocks and discussed them with our groups

- Traded and waited.

Some of my shares took off within months, others after years; four would die a slow death. Still believing they could be resuscitated, we have this bad habit of clinging on and not selling even if the share/s make up just a fraction of our portfolio. Psychologists believe our reluctance to take a loss is greater than accepting a gain. Very true!

TIP: If your stock falls, say by 10–20%, it may be a good idea to get out of it quickly. As long as you can show profits from other share trades in your tax return, you can also off-set losses.

Internet & media

The internet has now made investing easier. We simply click to buy, sell and research without having to talk to a single person or see a stockbroker. But the noise-info from financial ‘experts’ and economists has overwhelmed and confused many of you. Notice that their predictions are always accompanied by “maybe”, “most likely”, and/or “if management continues on this growth trajectory … “ Is this at all helpful??

The fact is nobody knows the future and profits generated the year before may not continue to the next. Have you picked up how the media, right on target, come out in droves when there’s a ‘bear’ market crash? They simply love the chance to go on TV or social media, telling you how much the shares have fallen and how much your superannuation has dropped. And they do the opposite when shares rise sharply in a ‘bull’ market – crying “it’s boom time’’ rattling off the stocks that have risen so much, it makes you sick that you didn’t ‘get in’ earlier!!

You know what? WE can do much much better.

Spend-control

First remove the fear of investing. I get it that most of you are clinging on to your hard-earned savings, earning a measly 1% interest. Let’s put spending in perspective.

In the past year, how much have you ladies spent on toiletries, fragrances, shampoos, and skin-care? Clothes, shoes, accessories? Cleaning products, cookware, kitchen gadgets? And how much have you men spent on electrical gizmos, computer games and equipment, and sports gear? Have we actually used every single item of stuff we’ve bought?

And then there’s eating out. Have we splurged on decadent breakfasts or lunches where only 1 serving costs more than an actual dinner? Have we bought presents thoughtlessly? We often give kids rubbish. Why not deposit money in their bank accounts?

Calculate all your misspends. Excluding food you’ve thrown away, what does it come to in the course of a year? We don’t give a thought to the money we’ve wasted but focus instead on the money we may lose!

My father and his friends would frown on such thinking. They invested wisely with thousands, but avoided supermarkets for Singapore’s (clean) wet markets – buying fruit and vegetables dollars cheaper per kilo.

Managed funds

You might be feeling complacent with your superannuation and other managed funds without getting more involved – but you should read your fund’s annual financial report. In particular:

- How your fund is performing

- Management and investment fees charged

- How and where your money is being invested.

- Invest in at least 1 online daily newspaper – they’re quick to alert of any argy-bargy with investment products.

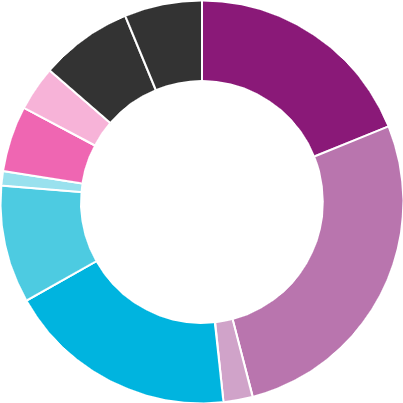

In a superannuation portfolio for example, you’ll usually see a pie-chart divided into coloured segments totalling 100%, showing where your money is being invested. Fund managers will alter percentages according to market changes in the short to medium-term. Here’s the pie-chart of my own super fund:

- Equities: Shares

- Private equity: International or Australian companies unlisted on stockmarkets

- Cash: Safe and secure with low risk, giving 2–3% interest

- Australian Fixed Interest: Bonds loans issued by the Australian govt – less volatile than shares but lower expected return

- International Fixed Interest: Bonds as above

- Credit Income: Covers a range of alternative debt investments

- Liquid Alternatives: Combines equities (shares), bonds, currencies & commodities

- Property: Office buildings, shopping centres and industrial estates; residential property, eg. apartments & retirement villages

- Infrastructure & real assets: Utilities & facilities providing essential community services.

TIP: Click the ‘Asset Classes’ link on your super fund’s website for more information.

Superannuation funds usually give you 4 investment options:

- ‘Cash‘

- ‘Capital Stable‘

- ‘Balanced‘

- ‘Growth‘ .

- Cash, Capital Stable and Balanced are safer for those in or near retirement, safeguarding income from regular allocated pension payments in any sharemarket crash.

- Growth means share investments for younger people with time to recover after a downturn. It’s still important to have the Growth option in all portfolios. When the market recovers, you don’t want to lose out by having all your capital staying in ‘safe’ mode.

TIP: If super funds bidding to buy Sydney Airport are right, there’ll be a substantial revival in both local and global travel.

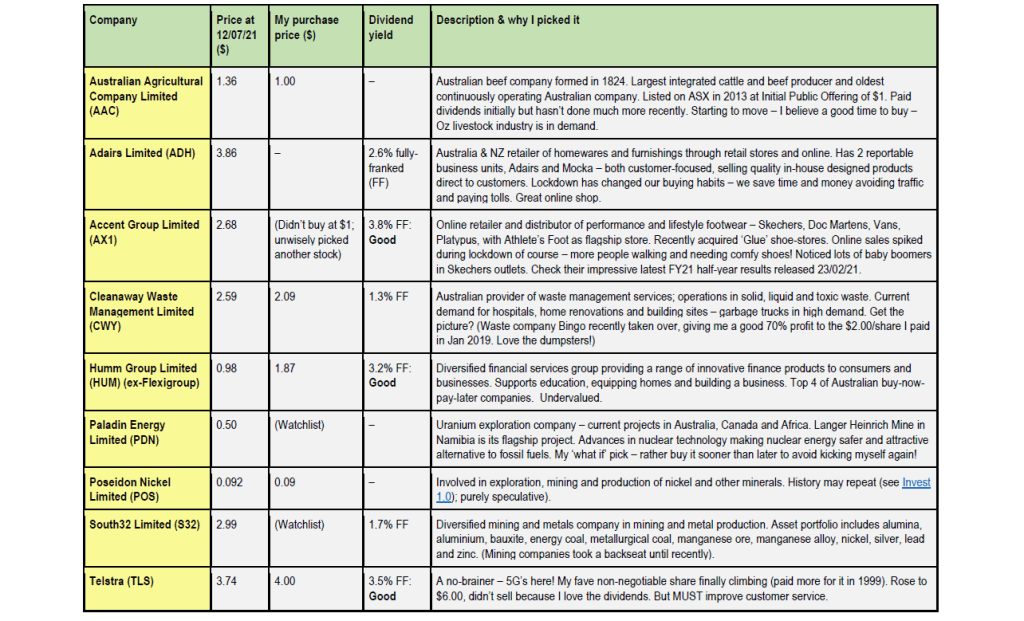

A few of my own ASX picks

FINAL TIPS:

Avoid travel stocks WEB, QAN and HLO at present – but keep watch. Every living being with money saved up will be packing their bags to cruise and fly once vaccination rates go up and that awful green spiked ball disappears from our screens.

Keep up with business news in your daily papers and online. Subscribe to at least 1 of Motley Fool’s many specifically targeted newsletters (eg. ‘Share Advisor’, Extreme Opportunities’, ‘Dividend Investor’ or ‘Hidden Gems’).

Observe. Talk to people. You’ll develop a keen sense of what the future holds. Therein lies the secret to share investing. Simple enough?

“TIME IS MONEY. BUT WEALTH IS THE RESULT OF TIME.”

The perfect quote from Scott Phillips of The Motley Fool to end my About Investing series (for now). I simply loved presenting it to you – GOOD LUCK!